Virtual Enterprise (VE) Coordinator, Mr. Power, extended an invitation to CNBC, a prominent financial and business news channel, to host “Smart Money” – a seminar on personal finance for seniors and VE students at Francis Lewis High School on December 7th. The event featured three distinguished guest speakers: Senior Economics Reporter Steve Liesman, CNBC Make It’s Money Reporter Kamaron McNair, and Deputy Personal Finance Editor CFP Kelli Grant. Topics covered included student debt, credit vs. debit cards, credit scores, investing vs. savings, and a holistic approach to managing money.

Principal Dr. Marmor emphasized the critical need for personal finance education in the school curriculum, underscoring the significance of the CNBC event in providing students with valuable insights for making informed financial decisions.

“I’ve heard it at the school leadership team meetings,” Dr. Marmor mentioned. “I heard it at multiple PTA meetings. I’ve even heard it at student government meetings. I’ve heard it at student focus groups. So over the past bunch of years, I’ve heard what I’m about to say from many different parts of the school community, which is that there is a glaring kind of hole in the curriculum, not just Francis Lewis, but in the city state curriculum, federal curriculum. There is no mandated piece of curriculum that is directed towards personal finance.”

In response to this demand on financial literacy VE program teacher Mr. Power organized the Smart Money event to bolster students’ understanding of money management, with a specific focus on seniors gearing up for college.

“We planned the event because it’s important to democratize financial literacy,” Mr. Power said. “I think that we as a department, as a school, [and] as adults, think that students at the high school and college level need to be able to make more informed financial decisions. In order to do that, we have to plan events like these to help expose them to the content that they can use as the foundation for research or for higher order conversations regarding money and money decisions.”

The seminar not only equipped students with financial knowledge but also complemented their economics classes, as highlighted by Senior Emily Gao. She expressed the need for a more targeted approach, stating that her AP Macroeconomics class, while valuable, lacks the specificity required for personal financial decision-making.

“I think [a financial literacy class] is a really great idea because not a lot of schools or classes would push up on these specific topics,” Senior Emily Gao stated. “As a student taking AP Macroeconomics last year, the concept is very general, it doesn’t touch up on my personal questions I have about my personal life. It is more about the economy in general and how the world works. In VE, we do touch up on the specific things that actually benefit us as we graduate. I feel like high school shouldn’t just be a space where we learn about these concepts but a space where we learn about how to apply these concepts.”

Students at FLHS are aware that these struggles they will face in life don’t get taught in high school.

VE students valued the CNBC event as an opportunity to get in touch with experienced mentors in relation to financial advice.

”I feel that way because they teach kids a lot of stuff that we don’t normally learn in high school,” stated VE CEO LangXi Xu. “The fact that they come and tell us these things that we are going to need in our life, and these people know the mistakes they’ve made previously and we’re having mentors that are very experienced and knowledgeable, it’ll definitely make us make smarter choices compared to if we never got to hear from them.”

While debt, such as credit card debt, is often viewed as purely negative, some debt can serve to be positive. As defined by Investopedia, a financial media website, “Good debt has the potential to increase your wealth, while bad debt costs you money with high interest on purchases for depreciating assets.”

As seniors in high school, many students are preparing to enter college, a decision that often comes with student loans and debt. However, Ms. McNaire argues that student debt can serve a positive function. “Growing as a person has made college for me invaluable,” she said.

“One, because it [student loans] is a little bit of an investment in terms of [the fact that] you need loans to go to college and you know that you’re going to college in order to make more money, so that’s an investment in your future,” Ms. McNaire said. “Also, if federal loans are coming with these protections, generally the interest rate is a lot, the average being around 5%, versus, a credit card, [which] you might have used for an emergency or something, but it’s not money that you’re gonna get back in general.”

However, along with credit cards comes credit card debt. As discussed by Capital One, credit card interest, which results from borrowing money, can lead to complications if the balance isn’t paid off in each billing cycle.

“You want to try to make sure, especially with credit cards, that you are not charging more than you can pay off in given billing periods so that you can help yourself understand how much you can spend [and] get used to paying that off in full,” Ms. Grant said.

In fact, credit card interests are known to be notoriously high, with the average credit card interest rates in America being 24.59% as reported by LendingTree. Thus, more than ever, it is important to pay attention to “cash flow” and spending habits.

“The best thing really is to pay attention to what you’re spending, you’ll hear people talk about it variously as a budget, cash flow,” Ms. Grant continued. “It really just comes down to figuring out what money is coming in, where it’s going and how well that aligns with where you want it to go. And if you are noticing that you spend a lot on your credit cards, more than you can pay off in a given period, that is a good sign to reassess your various habits.”

After participating in the CNBC event, students such as Xu were able to make a connection between what they learn in school “out of a textbook” to real life applications, as discussed in the seminar.

”This relates to my classes because we’re also working a lot on things like insurance, a lot of financial stuff,” said Xu. “[If] we learn more of this information, not only will it help us in real life, it will help us work with company work that we need to do. And it’s very good because in the future, we’ll definitely be interested in doing events like this and it definitely prepares us. Sometimes, instead of reading out of a textbook, we learn things that are actually happening in real life instead of things that are like a textbook that was made years ago. We’re learning the latest economic trends and the best choices for us as in the current moment.”

Emergency funds, or cash reinforcement, is important to ensure financial stability is maintained, even in the midst of a financial setback or to save money before investing.

“We talk about emergency funds, which is basically just cash that you’ve put aside for a rainy day, an emergency if you will, to be able to handle anything that comes your way.” Ms. Grant said. “People talk about it as being useful for small emergencies, like you have a flat tire or big ones like you lose your job and you need some money to live off of while you find another one. So even just getting started saving now, that helps you, because usually what you’ll hear financial advisors say is that you should have this emergency fund in place before you really focus your efforts on investing.”

Broadly speaking, with saving, there is widespread discussion about investing rather than saving. The argument is as follows: even while saving, a person can lose money due to inflation; however, if money were to be invested instead, there is a chance that the money can grow rather than decline.

“Generally, the Federal Reserve, which is a central bank that oversees policy and is tasked with keeping the economy moving, lets inflation come in at about 2% a year.” Ms. Grant said. “So if you think about that, if inflation is 2% and you have your money in a savings account that’s earning 1%, which was pretty common up until recently, your money losing value over time. If inflation is 2% and you are investing and you’re seeing, typical annual return somewhere around 6 or 7%, you are beating inflation and then some. So you’re not just preserving the value of your money, but you’re growing the value of your money.”

Although current seniors have learned about some personal finance from their economics classes, there are still many opportunities for them to build upon their current knowledge.

“I actually learned that from this event, starting early is the best option,” said VE Sales Johnny Zheng. “For example, investing early, starting these habits early, and being uncomfortable was one of the speakers said. So, in the future you’re more prepared, that’s the most important thing that I learned.”

Many seniors understand the fact that they are soon going to be on their own and that they need to learn this financial advice sooner than later.

“I thought the event was actually really beneficial for all of us especially since we’re heading into the real world and we’re all seniors,” Gao stated. “I really like the fact that Kelly and Kamaron both pushed up upon student debt and how it works. I really liked how Saket was asking questions regarding this and how he was showing his own experience. I feel like that’s something we need and it’s an aspect of this financial sector that us high school seniors and students miss during class.”

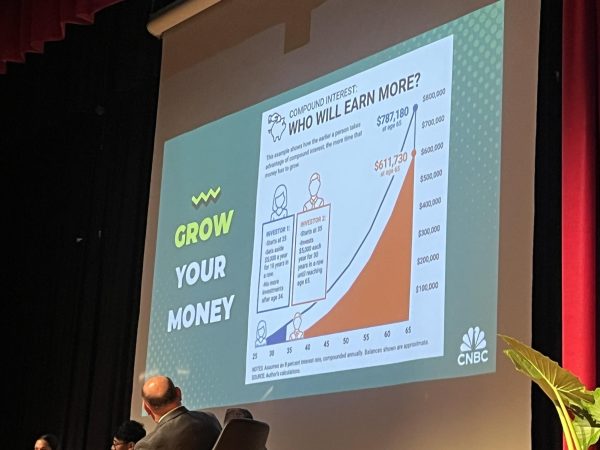

Especially, whether it’s investing or learning about personal finance, starting early to take advantage of compound interest is something young people especially, should take advantage of.

“I would say that the importance of starting early is really crucial for students to take away,” Ms. Grant said. “There are so many aspects of personal finance that get a little easier with time. Time is one of the greatest assets that young people have when it comes to their money, when you’re talking about investing for long term goals.”